HOTS Accountancy Class 12 Chapter 3 Reconstitution of a Partnership Firm – Admission of a Partner

Students of Class 12 Commerce should refer to the HOTS Accountancy Class 12 Admission of a Partner with solutions given below, this will help them to understand the concepts and related questions given in the Class 12 Accountancy textbook. It’s very important to understand High Order Thinking Skills questions and answers to get better marks in examinations.

Question: On what occasions does the need for valuation of goodwill arise?

Answer: Need of valuation of goodwill arises on the following occasions:-

(i) Change in profit sharing ratio of existing partners.

(ii) Admission of a partner.

(iii) Retirement of a partner.

(iv) Death of a partner.

Question: Why is it necessary to revalue assets and reassess liabilities at the time of admission of new partner?

Answer: It is necessary to revalue assets and reassess liabilities at the time of admission of new partners as if assets and liabilities are overstated or understated in the books then its benefits or loss should not affect the near partner.

Question: What is meant by sacrificing ratio?

Answer: Sacrificing ratio is the ratio in which old partners have agreed to sacrifice their share of profit in favour of the new partner. This ratio is calculated by deducting the new ratio from the old ratio.

Sacrificing Ratio = Old Ratio – New Ratio

Question: State two occasions when sacrificing ratio may be applied.

Answer: (i) On admission of a new partner.

(ii) On change on profit sharing ratio of existing partner.

Question: A business has earned average profit of Rs. 60,000 during the last few years. The assets of the business are Rs. 5,40,000 and its external liabilities are Rs. 80,000. The normal rate of return is 10%. Calculate the value of goodwill on the basis of capitalisation of super profits.

Answer: (i) Capital employed = Assets – Liabilities

= 540000 – 80000

= Rs. 460000

(ii) Normal Profit = Capital employed X Normal rate of return/100

= Rs. 460000 X 10/100 = 46000

(iii) Super Profit = Firm’s Average profit – Normal Profit

= 60000 – 46000

= 14000

(iv) Goodwill = Super profit X 100/ Normal rate of return

= 14000 X 100/ 10

= 140000

Question: Why should a new partner contribute towards goodwill on his admission?

Answer: Since a new partner gets his share of profit from old partners, he must compensate

the old partners for the share sacrificed by them. The amount of compensation

given by the new partner is known as goodwill.

Question: Why are assets and liabilities revalued on the admission of a new partner?

Answer: Assets and liabilities are revalued because the entire profit and loss due to their

revaluation is divided amongst the old partners in their old profits sharing ratio.

The new partner should not share such profit or loss because it belongs to the

period prior to his admission.

Question: Give the journal entry to distribute general reserve and profit and loss account

balance appearing on the liabilities side of the balance sheet.

Answer: General Reserve A/c Dr.

Profit & Loss A/c Dr.

To old partner’s capital A/c (In old ratio)

Question: Under what circumstances premium for goodwill paid by the incoming partner

would never be recorded in the books of account?

Answer: When the circumstances premium for the goodwill in cash to the old partners

privately outside the business no entries are passed for it.

Question: The capital of a firm of Arpit and Prajwal is Rs. 10,00,000. The market rate of return is 15% and the goodwill of the firm has been valued Rs. 1,80,000 at two years purchase of super profits. Find the average profits of the firm.

Answer: (i) Super profit = Value of goodwill /Number of years purchase

= 180000/2

= 90000

(ii) Normal Profit = Capital employed X Normal rate of return /100

= 1000000 X 15/ 100

= 150000

(iii) Average Profit = Normal Profit + Super profit

= 150000 + 90000

= 240000

Question: The average profits for last 5 years of a firm are Rs. 20,000 and goodwill has been worked out Rs. 24,000 calculated at 3 years purchase of super profits. Calculate the amount of capital employed assuming the normal rate of interest is 8 %.

Answer: (i) Super profit = value of goodwill/ number of years purchase

= 240000/3

= 80000

(ii) Normal Profit = Average profit – Super profit

= 20000 – 8000

= Rs. 12000

(iii) Capital Employee = Normal Profit X 100/ Normal rate of return

= 12000 X 100/8

= 150000

Question: X and Y should profits in the ratio of 3:1. They admit Z to one-third share in the

future profits. What will be the new profit sharing ratio?

Answer: Calculation of new profit sharing ratio:

Let total profit be = 1

Share given to Z = 1/3

Remaining share = 1-1/3 = 2/3

Now the old partners will share remaining profit in their old profit sharing

ratio:

Hence,

x’s share = 3/4 of 2/3 = 6/12 or ¾ * 2/3 = 6/12

y’s share = ¼ of 2/3 = 2/12 or ¼ * 2/3 = 2/12

z’s share = 1/3

Thus, the new profit sharing ratio of x, y and z will be:

= 6/12 : 2/12 : 1/3

= (6:2:4)/12 = 6:2:4 or 3:1:2

Question: A and B who shared profits in the ratio of 3:1 admit C as a partner for 1/5 share in

profits, which he requires equally from the old partners. What will be the new

profit sharing ratio?

Answer: Share of profit given to C = 1/5

Share acquired by C from A = ½ of 1/5 = 1/10

Share acquired by C from B = ½ of 1/5 = 1/10

Question: Rahul and Sahil are partners sharing profits together in the ratio of 4:3. They admit Kamal as a new partner. Rahul surrenders 1/4th of his share and Sahil surrenders 1/3rd of his share in favour of Kamal. Calculate the new profit sharing ratio.

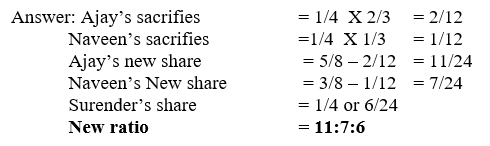

Question: Ajay and Naveen are partners sharing profits in the ratio of 5:3. Surinder is admitted in to the firm for 1/4th share in the profit which he acquires from Ajay and Naveen in the ratio of 2:1. Calculate the new profit sharing ratio.

Question: A and B share profits in the ratio of 2:1. C is admitted with 1/3 share in profits. C

acquires 2/3 of his share from A and 1/3 of his share from B. What will be new

profit sharing ratio?

Answer: Share of profit given to ‘C’ = 1/3 share

Share acquired by C from A = 1/3 * 2/3 = 2/9

Share acquired by C from B = 1/3 * 1/3 = 1/9

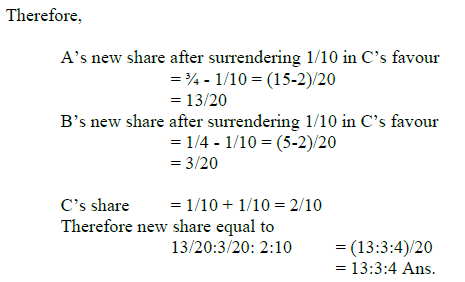

Question: A and B were partners sharing profits in the ratio of 3:2. A surrenders 1/6th of his share and B surrenders 1/4th of his share in favour of C, a new partner. What is the new ratio and the sacrificing ratio.

Question: Aarti and Bharti are partners sharing profits in the ratio of 5:3. They admit Shital for 1/4th share and agree to share between them in the ratio of 2:1 in future. Calculate new and sacrificing ratio.

Answer: Old ratio = 5:3

Shital = 1/4th Share

Let the profit be Rs. 1

Remaining profit = 1-1/4 =3/4

Arti : Babita = 2:1

Arti’s share = 3/4 X 2/3 = 1/2

Babita’s Share = 3/4 X 1/3 = 1/4

New Ratio = 1/2, 1/4, 1/4 Or 2:1:1

Sacrificing ratio = Old ratio – New ratio

Arti’s sacrifies = 5/8 – 2/4 = 1/8

Babita’s Sacrifies = 3/8 – 1/4 = 1/8

Sacrificing Ratio = 1:1Question: X and Y divide profits and losses in the ratio of 3:2. Z is admitted in the firm as a new partner with 1/6th share, which he acquires from X and Y in the ratio of 1:1. Calculate the new profit sharing ratio of all partners.

Answer: Old ratio = X:Y = 1:1

Z is admitted for 1/6th share which he acquire from X,Y in the ratio of 1:1

Since 1/6 X 1/2 = 1/12 from X and Y

X’s new ratio = 3/5 – 1/12 = 31/60

Y’s New ratio = 2/5 – 1/12 = 19/60

Z’s share = 1/6

New ratio = 31/60, 19/60,1/6 or 31:19:10Question: Rakhi and Parul are partners sharing profits in the ratio of 3:1. Neha is admitted as a partner. The new profit sharing ratio among Rakhi, Parul and Neha is 2:3:2. Find out the sacrificing ratio.

Answer:

Old ratio = Rakhi : Parul = 3:1

New ratio = Rakhi: Parul: Neha = 2:3:2

Rakhi’s sacrifice = 3/4 – 2/7 = 13/28

Parul’s sacrifice = 1/4 -3/7 = 5/28 (Gain)

So, Rakhi’s sacrifice 13/28th share and Parul is gaining to the extent of 5/28th share.

Question: X and Y are partners sharing profits in the ratio of 5:4. They admit Z in the firm for 1/3rd profit, which he takes 2/9th from X and 1/9th from Y and brings Rs. 1500 as premium. Pass the necessary Journal entries on Z’s admission.

Answer:

Cash A/C Dr. 1500

To premium A/C 1500

(cash brought in by Z for his share of goodwill)

Premium A/C Dr. 1500

To X’s capital A/C 1000

To Y’s Capital A/C 500

(Goodwill distributed among sacrificing partners in the ratio of 2:1.)Question: Ranzeet and Priya are two partners sharing profits in the ratio of 3:2. They admit Nilu as a partner, who pays Rs. 60,000 as capital. The new ratio is fixed as 3:1:1. The value of goodwill of the firm was determined at Rs. 50,000. Show journal entries if Nilu brings goodwill for her share in cash.

Answer:

Cash A/C Dr. 70000

To Nilu’s capital A/C 60000

To premium A/C 10000

(Cash brought in by new partner)

Premium A/C Dr. 10000

To Priya’s capital A/C 10000

(Amount of goodwill distributed among sacrificing partner in their sacrificing ratio.)Question: A and B are partners sharing profits equally. They admit C into partnership, C paying only Rs. 1000 for premium out of his share of premium of Rs. 1800 for 1/4th share of profit. Goodwill account appears in the books at Rs. 6000. All the partners have decided that goodwill should not appear in the new firms books.

Answer:

Cash A/C Dr. 1000

To premium A/C 1000

(Amount of goodwill brought in by C)

Premium A/C Dr. 1000

C’s capital A/C Dr. 800

To A’s capital A/C 900

To B’s capital A/C 900

(Rs. 1800 distributed among sacrificing partners in sacrificing ratio.)

A’s capital A/C Dr. 3000

B’s capital A/C Dr. 3000

To goodwill A/C 6000

(Old goodwill written off among old partners in old ratio.)Question: A and B are partners sharing profits in the ratio of 3:2. Their books showed goodwill at Rs. 2000. C is admitted with 1/4th share of profits and brings Rs. 10,000 as his capital but is not able to bring in cash goodwill Rs. 3000. Give necessary Journal entries.

Answer:

Cash A/C Dr. 10000

To C’s capital A/C 10000

(Cash brought in by C for his share of capital)

A’s capital A/C Dr. 1200

B’s Capital A/C Dr. 800

To goodwill A/C 2000

(Old goodwill written off among old partners in old ratio.)

C’s capital A/C Dr. 3000

To A’s capital A/C 1800

To B’s capital A/C 1200

(Adjustment of goodwill on admission of C)Question: Piyush and Deepika are partners sharing in the ratio of 7:3. they admit Seema as a new partner. The new ratio being 5:3:2. Pass journal entries.

Answer:

Cash A/C Dr. 4000

To premium A/C 4000

(Amount of goodwill brought in by new partner)

Premium A/C Dr. 4000

To Piyush’s capital A/C 4000

(Goodwill distributed among sacrificing partners in their sacrificing ratio.)Question: A and B are partners with capital of Rs. 26,000 and Rs. 22,000 respectively. They admit C as partner with 1/4th share in the profits of the firm. C brings Rs. 26,000 as his share of capital. Give journal entry to record goodwill on C’s admission.

Answer:

Cash A/C Dr. 26000

To C’s capital A/C 26000

(Amount of capital brought in by new partner.)

C’s capital A/C Dr. 7500

To A’s capital A/C 3750

To B’s capital A/C 3750

(C’s share of goodwill distributed among A and B)

Calculation of Hidden goodwill:-

Capital of A and B = 26000 + 22000

= 48000

C brings = 26000 for 1/4th share

Total capital of the firm = 26000 X 4/1

= 104000

Existing capital of the firm = 48000 + 26000

= 74000

Goodwill = 104000 – 74000

= 30000

C’s share of goodwill = 30000 X 1/4 = 7500Question: A and B are partners sharing profits in the ratio of 3:2. They admit C into partnership for 1/4th share. C is unable to bring his share of goodwill in cash. The goodwill of the firm is valued at Rs. 21,000. give journal entry for the treatment of goodwill on C’s admission.

Answer:

C’s capital A/C Dr. 5250

To A’s capital A/C 3150

To B’s capital A/C 2100

(C’s share of goodwill distributed among old partners in sacrificing ratio i.e. 3:2)

Question: A and B are partners with capitals of Rs. 13,000 and Rs. 9000 respectively. They admit C as a partner with 1/5th share in the profits of the firm. C brings Rs. 8000 as his capital. Give journal entries to record goodwill.

Answer:

Cash A/C Dr. 8000

To C’s capital A/C 8000

(Amount of capital brought in by new partner)

C’s capital A/C Dr. 2000

To A’s capital A/C 1000

To B’s capital A/C 1000

(Share of goodwill distributed among A and B in sacrificing ratio i.e. 1:1)

Calculation of Hidden Goodwill.

C brings 8000 for 1/5 share

Since total capital of the firm = 8000 X 5/1

= 40000

Existing capital of the firm = 13000 + 9000 + 8000

= 30000

Goodwill = 40000 – 30000

= 10000

C’s share of goodwill = 10000 X 1/5

= 2000Question: A, B and C were partners in the ratio of 5:4:1. On 31st Dec. 2006 their balance sheet showed a reserve fund of Rs. 65,000, P&L A/C (Loss) of Rs. 45,000. On 1st January, 2007, the partners decided to change their profit sharing ratio to 9:6:5. For this purpose goodwill was valued at Rs. 1,50,000.

The partners do not want to distribute reserves and losses and also do not want to record goodwill.

You are required to pass single journal entry for the above.

Answer:

C’s Capita; A/C Dr. Rs. 25, 500

To A’s Capital A/C Rs. 8,500

To B’s Capital A/C Rs. 17,000

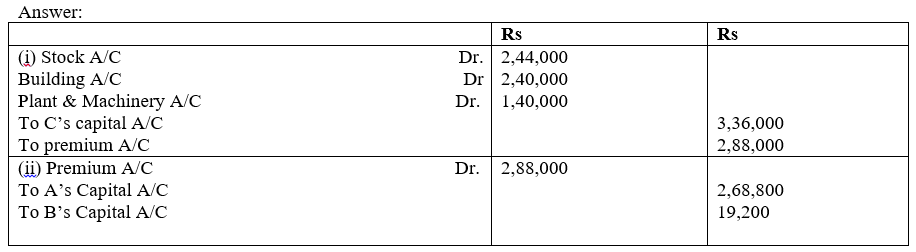

Question: A and B were partners in the ratio of 3:2. They admit C for 3/13th share. New profit ratio after C’s admission will be 5:5:3. C brought some assets in the form of his capital and for the share of his goodwill.

Following were the assets:

Assets Rs.

Stock 2,44,000

Building 2,40,000

Plant and Machinery 1,40,000At the time of admission of C goodwill of the firm was valued at Rs. 12,48,000.

Pass necessary journal entries.

Question: X, Y and Z are sharing profits and losses in the ratio of 5:3:2. They decide to share future profits and losses in the ratio of 2:3:5 with effect from 1st April, 2002. They also decide to record the effect of the reserves without affecting their book figures, by passing a single adjusting entry.

Book Figure

General Reserve Rs. 40,000

Profit 2 loss A/C (Cr) Rs. 10,000

Advertisement Suspense A/C(Dr) Rs. 20,000

Pass the necessary single adjusting entry.

Question: X and Y are partners sharing profits in the ratio of 3:1. They admit Z as a partner.

X surrenders 1/3rd of his share and Y 1/4th of his share in favour of Z. What will be

new profit sharing ratio?

Answer: x : y – 3 : 1, z admitted

x -> 1/3 * ¾ = ¼ (x surrender 1/3 of his share)

y -> 1/4 * 1/4 = 1/6 (y surrender 1/4 of his share)

Therefore, z’s share -> ¼ + 1/16 = (4+1)/16 = 5/16

New profit sharing ratio:

x = ¾ – ¼ = 2/4

y = 1/4 – 1/16 = (4-1)/16 = 3/16

z = 5/16

Therefore, 2/4 : 3/16 : 5/16

→ (8:3:5)/16

→ 8:3:5

Question: P and q are partners sharing profits in the ratio of 5:3. R is admitted and the new

ratio is 4:3:2. What will be sacrificing ratio?

Answer:

Question: M and N are partners. P is admitted for ¼ shares. What is the ratio in which M and

N will sacrifice their share in favour of P?

Answer: Profit distributed equally.

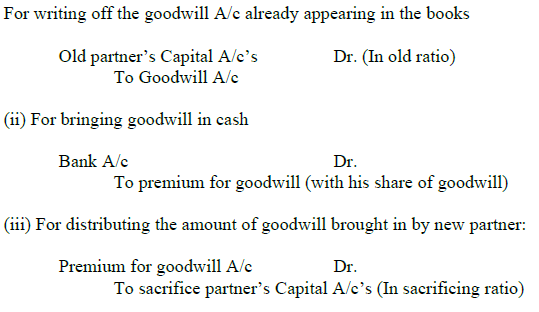

Question: Explain the accounting treatment of Goodwill when goodwill account already

appears in the books of the firm and new partner brings his share of goodwill in

cash.

Answer:

Question: Explain the accounting treatment of Goodwill when new partner cannot bring his

share of goodwill in cash.

Answer: New Partner’s Capital A/c Dr. (with his share of goodwill)

To sacrificing Partner’s Capital A/c’s (In sacrifice ratio)

Question: K.L and M partners sharing in the ratio of 3:2:1. They admit N for 1/6th share. It is

agreed that M would retain his original share. Calculate new ratios and sacrificing

ratios.

Answer: Calculation of New profit Sharing Ratio:

N’s share = 1/6; M’s share = 1/6

Remaining share for K and L = 1 – (1/6 + 1/6) = 4/6

This will be divided between K and L in their old ratio i.e., 3 : 2

Hence, the new share of K = 3/5 * 4/6 = 12/30

New share of L = 2/5 * 4/6 = 8/30

The new ratio of K, L and M, N = 12/30 : 8/30 : 1/6 :1 /6 or

= 12 : 8 :5 : 5

Calculation of sacrifice ratio:-

Sacrifice made by K = 3/6 – 12/30 = 3/30

Sacrifice made by L = 2/6 – 8/30 = 2/30

Sacrifice made by M = NIL

Thus, sacrificing ratio among K, L and M = 3 : 2 : 0

Question:

Question: A,B and C are partners, sharing profits in the ratio of 4:3:2. D is admitted for 2/9

share of profits and bring Rs. 30,000 and Rs. 10,000 for his share of goodwill. The

new profit sharing ratio will be A:B:C:D, 3:2:2:2. Journalise the above

arrangement in the books

Answer:

Working Note:- Calculation of sacrificing ratio :-

Sacrificing ratio = Old ratio – New ratio

Thus, A’s sacrifice ratio = 4/9 – 3/9 = 1/9

B’s sacrifice ratio = 3/9 – 2/9 = 1/9

C’s sacrifice ratio = 2/9 – 2/9 = 0

As, C has not made any sacrifice, therefore he will not be entitled to any amount

of goodwill brought in by new partner.

A & B have sacrificed in equal proportion, therefore they will get equal share in

the goodwill brought in by D.

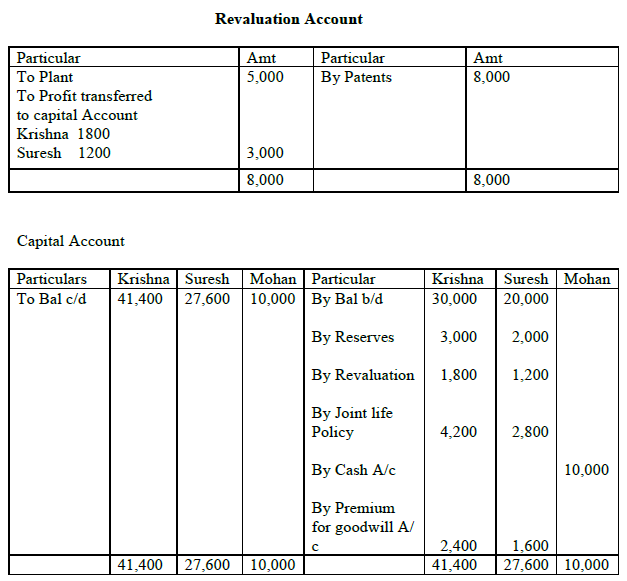

Question: Krishna and Suresh are partners in a firm sharing profits in the ratio of 3:2

On that data Mohan is admitted as a partner for 1/5 share on the following terms.

(a) He is to contribute Rs. 14,000 as his share of capital which includes his share of

premium for goodwill.

(b) Goodwill it valued at 2 years purchase of the average profits of the last four years

which were Rs. 10,000; Rs. 9,000; Rs. 8,000 and Rs. 13,000 respectively.

(c) Plant to written down to Rs. 25,000 and patents written up by Rs. 8,000.

(d) A joint life policy taken in the name of the partner for Rs50000 on which premiums

have been paid has a surrender value of Rs. 7,000. Prepare Revolution Account,

Partners’ capital accounts and the balance sheet of the new firm.

Answer:

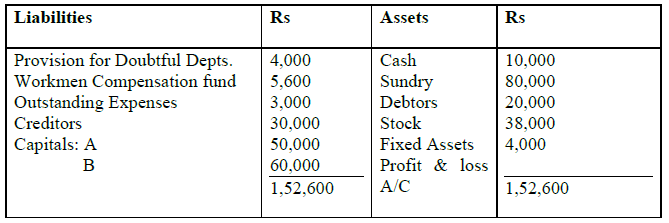

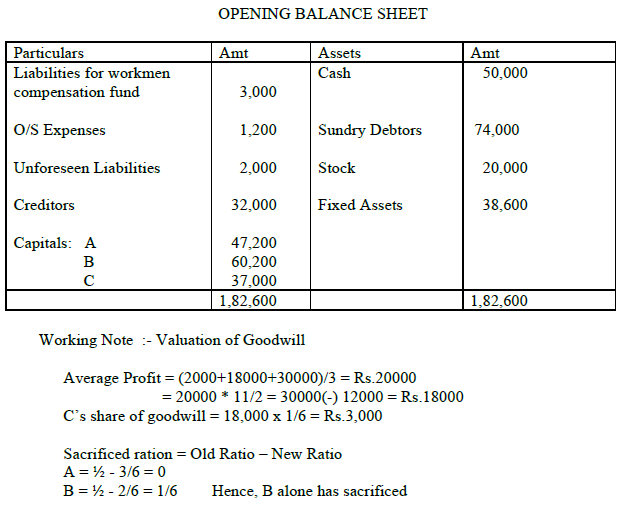

Question: A and B are partners in a firm. Their balance sheet as on 31/12/1993 was as follows.

C was taken into partnerships as from 01.01.94. C brought Rs. 40,000 as his capital but he is

unable to bring any amount for goodwill. New profit sharing ratio is 3:2:1. Following terms

were agreed upon:

1. Claim on account of workmen’s Compensation is Rs. 3,000.

2. To write off Bad Debts amounting to Rs. 6,000.

3. Creditors are to be paid Rs. 2,000 more.

4. Rs. 2,000 be provided for an unforeseen liability.

5. Outstanding expenses be brought down to Rs. 1,200

6. Goodwill is valued at 1 ½ years purchase of the average profits of last three years, less

Rs. 12,000. Profits of 3 years amounting to Rs. 12,000; Rs. 18,000, and Rs. 30,000.

Prepare Journal Entries, capital accounts and balance sheet.

Answer:

Question: Following is Balance sheet of A and B who share profits in the ratio of 2:1

Answer:

They admitted C into partnership on this date. New profit sharing ratio is agreed as

3:2:1. C brings in proportionate capital after the following adjustments.

1. C brings in Rs. 10,000 in cash as his share of Goodwill.

2. Provision for doubtful debts is to be reduced by Rs. 2,000

3. There is an old typewriter valued Rs. 2,600. It does not appear in the books of

the firm. It is now to be recorded.

4. Patents valueless.

5. 2 % discount is to be received from creditors. Prepare revaluation A/C, Capital

A/Cs and Balance Sheet.

Answer:

Working Notes:

1. Sacrifice Ratio = Old Ratio – New Ratio

Sacrifice by A = old 2/3 – new 3/6 = 1/6

Sacrifice by B = old 1/3 – new 2/6 = 0

Since B has not made any sacrifice, the ratio amount of premium for goodwill

brought in by C will be credited to A.

2. C’s Capital is not given in the question. He will bring in capital proportionate to

his share of profits. C is given 1/6th share of profits, balance 5/6th is shared by A

and B. Total capital of A and B after all adjustments is Rs.60,000 + 35,000

= 95,000.

Thus, for 5/6th share of profits the capital = 95,000

Then total capital of the firm = 95,000 * 6/5 = Rs.1,14,000

Therefore C’s capital for 1/6th share profits = 1,14,000 * 1/6 = Rs.19,000

3. Calculation of balance at bank:

Amt. of Cash brought in by C as goodwill = 10,000

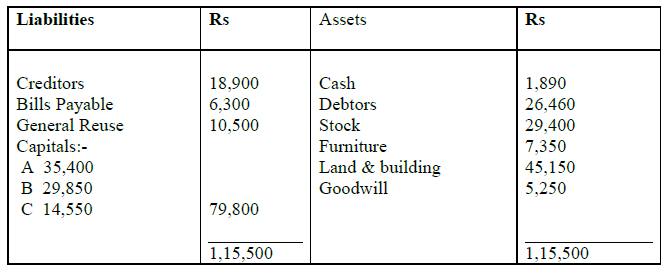

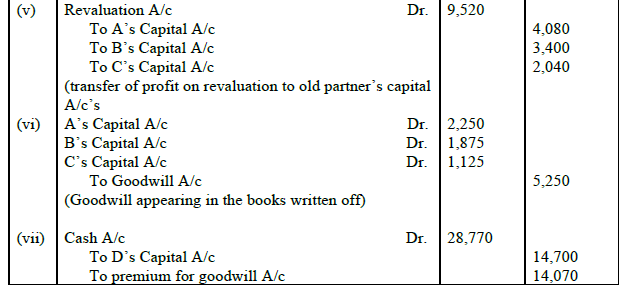

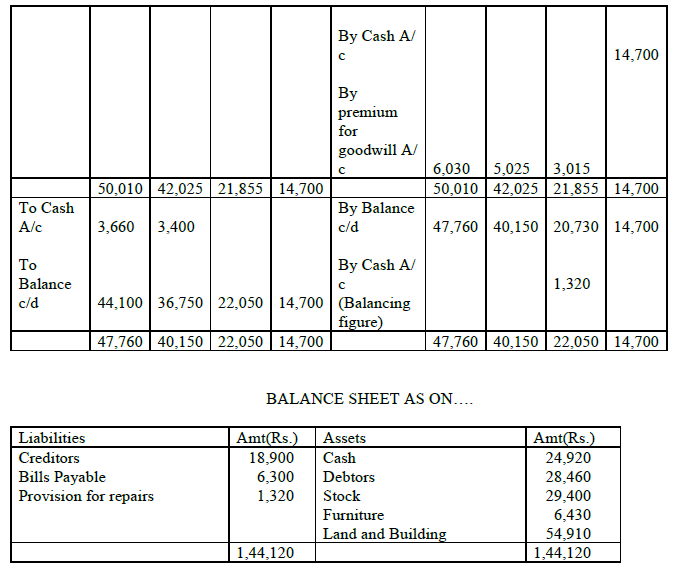

Question: Following is the balance sheet of A,B and C sharing profits and losses in

Proportion of 6:5:3 respectively.

They agreed to take D into partnership and give him 1/8 the share on the following terms.

(1) That furniture be depreciated by Rs. 920.

(2) An old customer, whose account was written off as bad, has promised to pay

Rs 2,000 in full settlement of his full debt.

(3) That a provision of Rs. 1,320 be made for outstanding repair bills.

(4) That the value of land and building have appreciated be brought up to Rs.

54,910

(5) That D should bring in Rs. 14,700 as his capital.

(6) That D should bring in Rs. 14,070 as his share of goodwill.

(7) That after making above adjustment, the capital accounts of old partners be

adjusted on the basis of the proportion of D’s capital to his share in business

i.e. actual cash to be paid off or brought in by the old partners, as the case may

be.

Prepare Journal Entries and prepare the balance sheet of new firm.

Answer:

D bring in Rs.14,700 as capital according to his 1/8th share of profit. Therefore,

according to D’s capital, the total capital of the new firm will be:

= 14,700 * 8/1 = Rs.1,17,600

Therefore A’s Capital in new firm = 1,17,600 * 6/16 = Rs.44,100

B’s Capital in new firm = 1,17,600 * 5/16 = Rs.36,750

C’s Capital in new firm = 1,17,600 * 3/16 = Rs.22,050

D’s Capital in new firm = 1,17,600 * 2/16 = Rs.14,700