Notes Chapter 2 Theory of Consumer Behaviour

Class 12 students can refer to Chapter 2 Theory of Consumer Behaviour notes given below which is an important chapter in the class 12 Economics book. These notes and important questions and answers have been prepared based on the latest CBSE and NCERT syllabus and books issued for the current academic year. Our team of Economics teachers has prepared these notes for class 12 Economics for the benefit of students so that you can read these revision notes and understand each topic carefully.

Theory of Consumer Behaviour Notes Class 12 Economics

Refer to the notes and important questions given below for Theory of Consumer Behaviour which is really useful and has been recommended by Class 12 Economics teachers. Understanding the concepts in detail and then solving questions by yourself will help you to learn all topics given in your NCERT Books.

Consumer is an economic agent who consumes final goods or services for a consideration.

Thus Consumer behaviour is the study of how individual customers, groups or organizations select, buy, use, and dispose ideas, goods, and services to satisfy their needs and wants. It refers to the actions of the consumers in the marketplace and the underlying motives for those actions.

Utility is want satisfying power of a commodity. There are two types:-

* Total utility is the total satisfaction derived from consumption of given quantity of a commodity at a given time. In other words, It is the sum total of marginal utility.

* Marginal Utility is the change in total utility resulting from the consumption of an additional unit of the commodity. In other words, it is the utility derived from each additional unit.

Law of Diminishing Marginal Utility: As consumer consumes more and more units of commodity the Marginal utility derived from each successive units go on declining. This is the basis of law of demand.

Consumer’s Bundle is a quantitative combination of two goods which can be purchased by a consumer from his given income.

Law of Equi-Marginal utility- It states that when a consumer spends his income on different commodity he will attain equilibrium or maximize his satisfaction at that point where ratio between marginal utility and price of different commodities are equal and which in turn is equal to marginal utility of money.

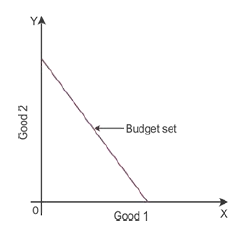

Budget set is quantitative combination of those bundles which a consumer can purchase from his given income at prevailing market prices. The group of all the bundles which the consumer is able to buy with his/her income at the prevailing prices in the market is called the budget set of a consumer. The budget set of a consumer is basically a collection of all bundles of goods and services which a consumer can purchase by using the available income.

Consumer Budget:- A budget constraint represents all the combinations of goods and services that a consumer may purchase given current prices within his or her given income. Consumer Budget states the real income or purchasing power of the consumer from which he can purchase certain quantitative bundles of two goods at given price. It means, a consumer can purchase only those combinations (bundles) of goods, which cost less than or equal to his income.

Budget Line: A graphical representation of all those bundles which cost the amount just equal to the consumer’s money income gives us the budget line. The budget line represents two different combinations of goods which a consumer can purchase with the given income and prices of commodities.

For example;-

Q1 be the amount of Good 1, Q2 be the amount of Good 2, P1 be the price of Good 1, P2 be the price of Good 2, P1q1 = Total money spent on Good 1, P2q2 = Total money spent on Good 2. Therefore, the equation of the budget line will be p1q1 + p2q2 = X. The budget set can be shown in the below diagram:

Budget line always slope downwards so that consumer can increase the consumption of Good 1 only by decreasing the consumption of Good 2. If consumers desire to have one additional unit of Good 1, then they can only have that additional unit if they manage to give up some quantity of other good. Consumers have limited income. They have to decide whether to spend on either Good 1 or Good 2.

Monotonic Preferences: Consumer’s preferences are called monotonic when between any two bundles, one bundle has more of one good and no less of other good as it offers him a higher level of satisfaction.

Change in Budget Line: There can be parallel shift (leftwards or rightwards) due to change in income of the consumer and change in price of goods. A rise in income of the consumer shifts the budget line rightwards and vice-versa. In case of change in price of one good, there will be rotation in the budget line. Fall in price cause outward rotation due to rise in purchasing power and vice-versa.

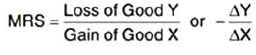

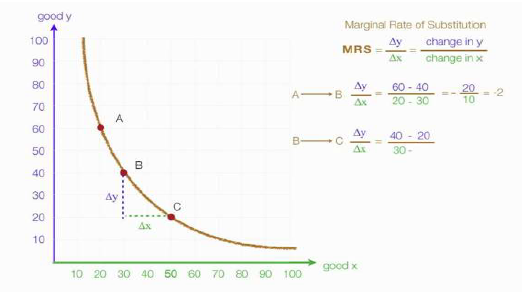

Marginal Rate of Substitution (MRS) : It is the rate at which a consumer is willing to substitute (good Y/ good X) one good to obtain one more unit of the other good. Generally, It is the slope of indifference curve.

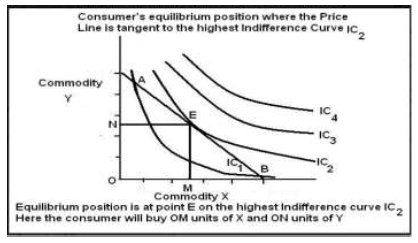

Indifference Curve: It is a curve showing different combination of two goods, each combinations offering the same level of satisfaction to the consumer.

Characteristics of IC

1. Indifference curves are negatively sloped (i.e. slopes downward from left to right).

2. Indifference curves are convex to the point of origin. It is due to diminishing marginal rate of substitution.

3. Indifference curves never touch or intersect each other. Two points on different IC cannot give equal level of satisfaction.

4. Higher indifference curve represents higher level of satisfaction.

Preference of consumer is governed by monotonic preferences. Monotonic Preferences refers to a situation, where the consumer will prefer more of a commodities than the combination providing lesser commodities. OR A consumer’s preferences are monotonic if and only if between any two bundles, the consumer prefers the bundle which has more of at least one of the goods and no less of the other good as compared to the other bundle.

Consumer’s Equilibrium: A consumer is said to be in equilibrium when he maximizes his satisfaction, given his money income and prices of two commodity. He attains equilibrium at that point where the slope of IC is equal to the slope of budget line.

Marginal Rate Of Substitution:-

Marginal Rate Of Substitution MRS refers to the rate at which the consumer substitute one good to obtain one more unit of the other good. The slope of the Indifference curve is

MRS = Δy/Δx •MR

MRS is never constant, it varies over the IC. As we move along Indifference Curve, MRS falls also called Diminishing Marginal rate of substitution.

Quantity Demanded: It is that quantity which a consumer is able and is willing to buy at particular price and in a given period of time.

Determinants of Demand:

a) Price of Good

b) Income of Consumers

c) Taste & Preference of Consumer

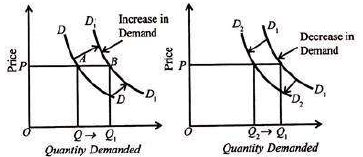

Change of Demand :

a) Change in quantity demanded or Movement along Demand curve

b) Change in Demand or Shift in Demand

Market Demand: It is the total quantity of the commodity demanded in the market by all consumers at different prices at a point of time.

Demand Function: It is the functional relationship between the demand for a commodity and factors affecting demand.

Law of demand: The law states that when all other thing remains constant then there is inverse relationship between price of the commodity and quantity demanded of it. That is, higher the price, lower the demand and lower the price, higher the demand.

Change in Demand: When demand changes due to change in any one of its determinants other than the price.

Change in Quantity Demanded: When demand changes due to change in its own price keeping all other factors constant.

Demand curve and demand schedule: The tabular presentation of price and quantity. It is called demand schedule and a demand curve is the graphical representation of the demand schedule.

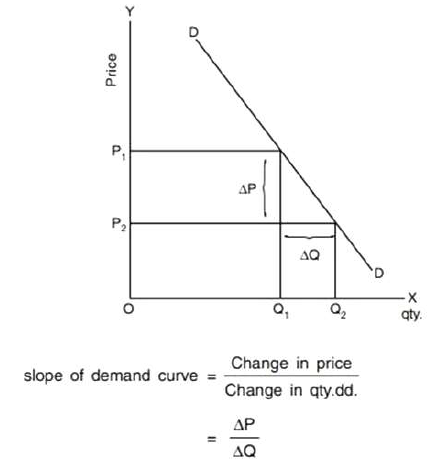

Demand curve and its slope:

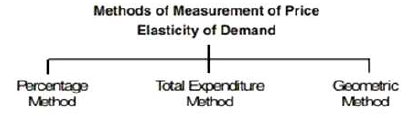

Price Elasticity of Demand: Price Elasticity of Demand is a measurement of change in quantity demanded in response to a change in price of the commodity.

Percentage Method:

E = ΔQ/ΔP × P/Q

EP → Elasticity of Demand

ΔQ → Change in quantity

DP → Change in price

P → Initial price

Q → Initial Quantity

Or

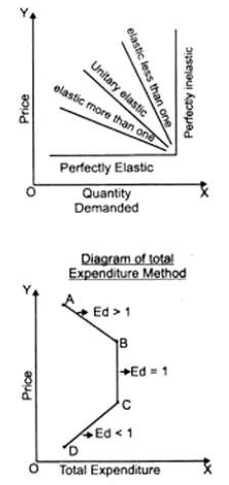

Total Expenditure Method : It measures price elasticity of demand on the basis of change in total expenditure incurred on the commodity by a household due to change in its price.

There are three conditions :

1. Ed=1 When due to rise or fall in price of a good, total expenditure remains unchanged.

2. Ed >1 When due to fall in price, total expenditure goes up and due to rise in price, total expenditure goes down.

3. Ed <1 when due to fall in price, total expenditure goes down and due to rise in price, total expenditure goes up.

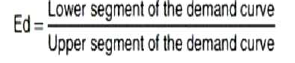

Geometric Method : Elasticity of demand at any point is measured by dividing the length of lower segment of the demand curve with the length of upper segment of demand curve at that point.

The value of ed is unity at mid point of any linear demand curve.

Diagram to show Geometric or point method:

Elasticity of demand at given point.

D is midpoint of the demand curve.

Degree uf Price Elasticity

Factors influencing Price elasticity of Demand

(a) Nature of the Commodity.

(b) Availability of Substitute goods.

(c) Income level of the consumer.

(d) Price level of the commodity.

(e) Time Period.

(f) Different use ofthe commodity.

(g) Behaviour ofthe consumer.

(h) Postponement of consumption.