Notes for Class 11 Accountancy Chapter 4 Recording of Transactions II

Students can refer to Notes for Class 11 Accountancy Chapter 4 Recording of Transactions II given below. These notes have been prepared keeping into consideration the latest syllabus and examination guidelines issued by CBSE and NCERT. Class 11 Chapter 4 Recording of Transactions II Notes is important to understand the topic and solve all questions given in DK Goel Class 11 Textbook

Unit at a Glance:

• Introduction

• Meaning and Importance of Ledger.

• Format of Ledger.

• Postings from Journal.

• Postings from Cash Book and other Subsidiary Books.

• Closing and Balancing of Ledger Accounts.

• Trial Balance – Meaning, objectives and Preparation.

• Meaning and importance of Suspense A/c.

• Bank Reconciliation Statement

• Generally students commits mistakes please avoid it

• Questions

“Ledger is a book which contains all accounts of the business enterprise whether Personal, Real or Nominal.”

INTRODUCTION

After recording the business transaction in the Journal or special purpose Subsidiary Books, the next step is to transfer the entries to the respective accounts in the Ledger. Ledger is a book where all the transactions related to a particular account are collected at one place.

LEDGER

Definition: The Ledger is the main or principal book of accounts in which all the business transactions would ultimately find their place under various accounts in a duly classified form.

According to L.C. Cropper,” The book which contains a classified and permanent record

of all the transactions of a business is called the ledger.”

By this classification / collective effect we are able to know the following –

How much amount is due from each customer and how much amount the firm has to pay to

each supplier/ creditor.

⇒ The amount of Purchases and Sales during a particular period.

⇒ Amount paid or received on account of various items.

⇒ Ultimate position of Assets and Capital.

⇒ For the preparation of Trial Balance which helps in ascertaining the Arithmetic Accuracy of the Accounts.

PERFORMA OF LEDGER

• Each ledger account is divided into two equal parts.

Left Hand Side–Debit side (Dr)

Right Hand Side– Credit side (Cr)

POSTING IN THE LEDGER

This will be dealt separately from Journal Entries and each Subsidiary Book.

Case I – Posting from Journal Entries.

♦ If an account is debited in the journal entry, the posting in the ledger should be made on the debit side of that particular account. In the particular column the name of the other account (which has been credited in the Journal entry) should be written for reference.

♦ For the A/c credited in the Journal entry, the posting in the ledger should be made on the credit side of that particular A/c. In the particulars column, the name of the other account that has been debited (in the Journal entry) is written for reference.

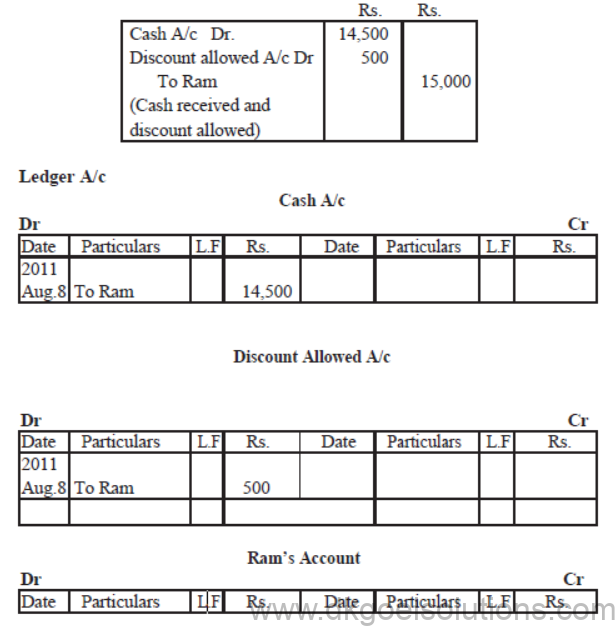

Example 2: Compound Journal Entry.

Received Rs.14,500 in full settlement of a debt of Rs. 15,000 from Ram on Aug 8, 2011.

SULUTION – Journal Entry

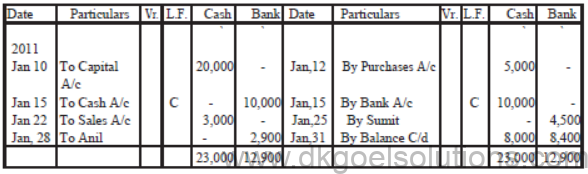

Case II. – Ledger Postings from Cash Book

♦ Important Points

(1) Cash Book itself serves as a cash A/c also, therefore when cash book is maintained, cash A/c is not opened in the ledger.

(2) When Bank column is maintained in the Cash Book, Bank A/c is also not opened in the ledger.

The Bank column itself serves the purpose of Bank A/c.

(3) Opening and closing balances of Cash Book will not be entered in the ledger anywhere.

(4) As Cash Book serves the purpose of Cash/Bank A/c, it means that, only the second A/c (other than Cash A/c or Bank A/c) is to be opened in the ledger and posting is to be made for each entry in the Cash Book.

I llusration: Given some Cash Book entries post there into ledger A/c

SOLUTION:

15th Jan. entry will not be posted (Contra Entry) Closing Balance will not be posted in the ledger

Case III- Ledger posting from Purchases book

Journal Entry for Credit Purchases is

Purchases A/c Dr

To Supplier A/c

Therefore the rules of posting from Purchases Book are.

(1) The total of the Purchases book will be posted to the Debit side of Purchase A/c and the w ords “To Sundries as per Purchase Book” will be written in the particulars column.

(2) Each of the Supplier’s A/c will be Credited and the words. “By Purchases A/c” will be written in the particulars column.

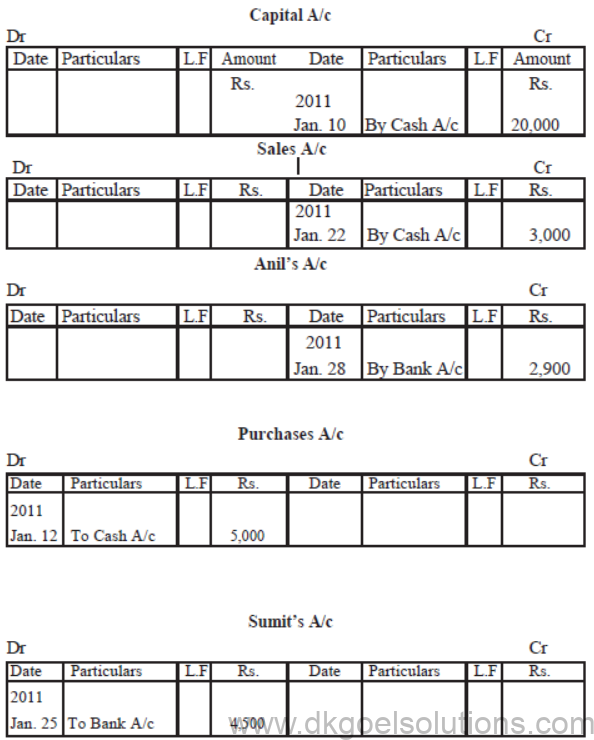

Illustration:

SOLUTION: LEDGER A/C s

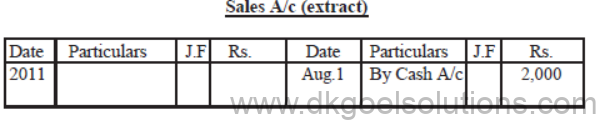

Case IV- Ledger Postings from Sales Book

Journal Entry for Credit sales is

Customer A/c Dr.

To Sales A/c

Hence rules for posting from sales Book are

1. Total of the Sales Book will be posted to the credit side of sales A/c by writing the words

“By Sundries as per Sales Book”

2. Customer’s personal A/c s are debited by writing the words “To Sales A/c”

Case V- Ledger Postings from Purchase Return Book

Journal Entry for purchase Return is

Personal A/c of Supplier a/c Dr

To Purchase Return A/c.

Hence the rules for posting are.

1. Supplier’s A/c (to whom the goods are returned) is debited by writing the words “To Purchase Return A/c”)

2. The total of the Purchases return Book is credited to the Purchases Return A/c by writing the w ords “By Sundries as per Purchases Return Book”.

Case VI – Ledger Postings of Sales Return Book

Journal Entry for the Sales Return is –

Sales Return A/c Dr

To Customer A/c

Hence the Rules for Posting are

(1) Individual Customer’s A/C s by whom the goods are returned are credited by writing the words “By Sales Return A/c”.

(2) The total of the Sales Return Book is posted to the Debit of Sales Return A/c by writing the words. “To Sundries as per Sales Return Book”.

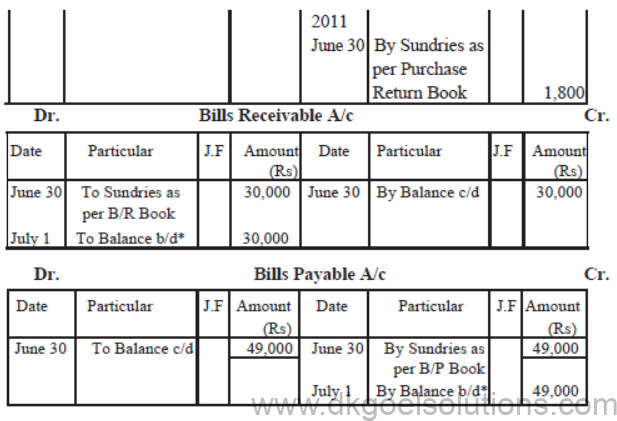

a. Ledger Postings from Bills Receivable Book.

Bills Receivable book shows the names of the persons from whom the Bills are received.

Therefore the Journal Entry is

B / R A/c Dr.

To Personal A/c

Hence. (1) Posting will be done on the Credit side of the Personal A/cs by writing the words. “By Bills Receivable A/c”.

(2) The total of the Bills Receivable Book will be posted to the debit side of Bills Receivable

A/c by writing the words “To Sundries as per Bills Receivable Book”.

b. Ledger Postings of Bills Payable Book

Bills payable is a liability, therefore the Journal Entry is

Personal A/c Dr

To Bills Payable A/c.

Hence the rules of Posting are

1. Personal A/C s will be debited by writing the words. “To Bills Payable A/c”.

2. Total of the Bills Payable Book will be posted to the credit of Bills Payable A/c by writing

“By Sundries as per Bills Payable Book”.

Normally after every month or whenever a businessman is interested in knowing the position of various A/C s, the accounts are balanced. Various steps for this purpose are .

(1) Debit and Credit sides of each A/c are totalled.

(2) The difference between the two sides is written on the side which is shorter so as to make their totals equal.

(3) The words “Balance C/d” i.e. the balance carried down and written against the amount of difference.

(4) In the next period, the balance is brought down on the other side by writing the words ‘Balance b/d’.

(5) If the Debit side exceeds the Credit Side the difference is a Debit Balance whereas.

(6) If the Credit side exceeds the Debit side the difference is a Credit Balance.

• GENERALLY STUDENTS COMMITS MISTAKES PLEASE AVOID :-

1. Debit Balance of a Personal A/c means the person is a Debtor of the firm whereas Credit Balance of a Personal A/c indicates that the person is a Creditor of the firm.

2. Real A/c s (which include Cash and all other Assets A/c s) will usually show Debit Balances.

3. Nominal A/C s (A/c s of Income and Expenses) are transferred to Trading and Profit and Loss A/c of the firm at the end of the Accounting Period.

4.Debit Balance of any A/c means an Asset or an Expense whereas Credit Balance means a liability, Capital or Income earned.

TRIAL BALANCE

I Meaning – When posting of all the transactions into the Ledger is completed and accounts are balanced off, then the balance of each account is put on a list called Trial Balance.

II Definition – Trial Balance is the list of debit and credit balances taken out from ledger. “It also includes the balances of Cash and bank taken from the Cash Book”.

III Preparation – Steps (Only Balance Method)

(1) Ledger A/Cs which shows a debit balance is put on the Debit side of the trial balance.

(2) The A/c’s Showing credit balance are put on the Credit side of the Trial Balance.

(3) Accounts which show no balance i.e. whose Debit and Credit totals are equal are not entered in Trial Balance.

(4) Then the two sides of the Trial Balance are totaled. If they are equal it is assumed that there are no arithmetical error in the posting and balancing of Ledger A/cs.

Objectives or Functions of Trial Balance

• It helps in ascertaining the arithmetical accuracy of ledger accounts.

• Helps in locating errors.

• Provides the summary of Ledger A/cs.

• Helps in the preparation of Final A/cs.

Recording in the journal and subsidiary Books, Posting into the Ledger and Preparation of Trial Balance can be clearly understood with the help of the example given on next pages.

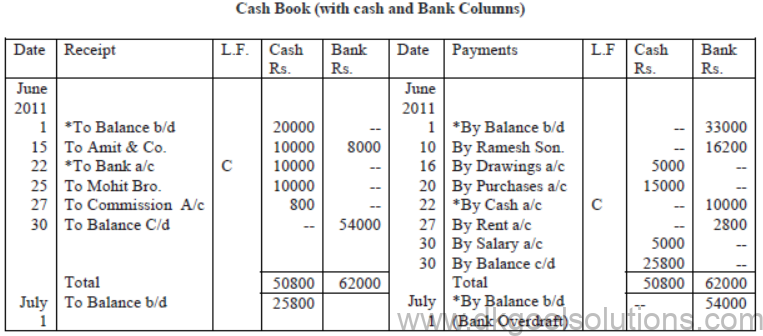

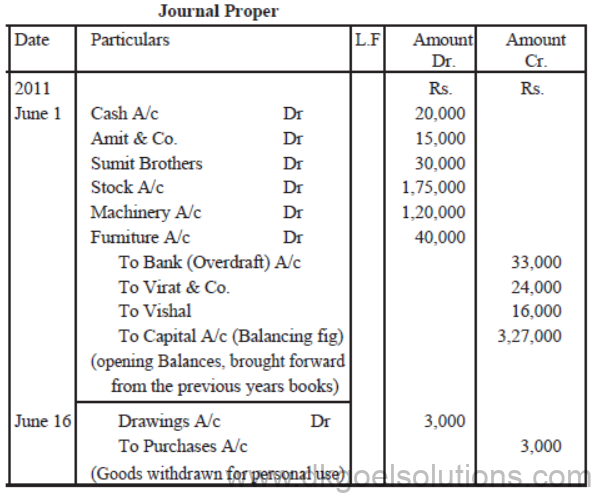

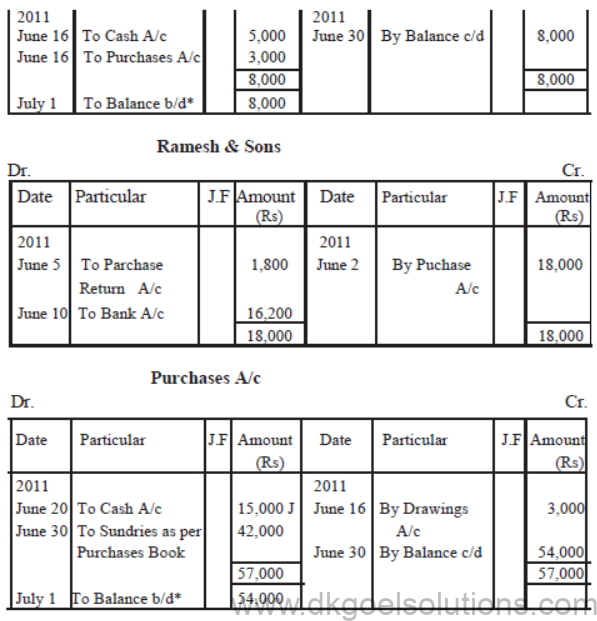

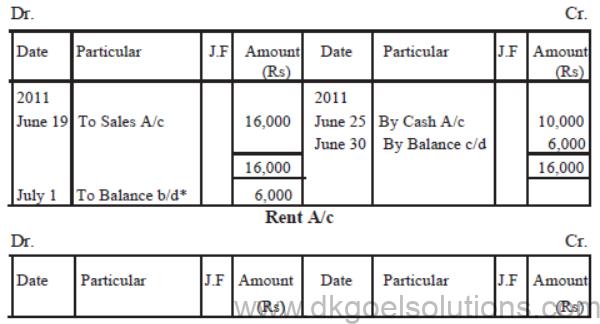

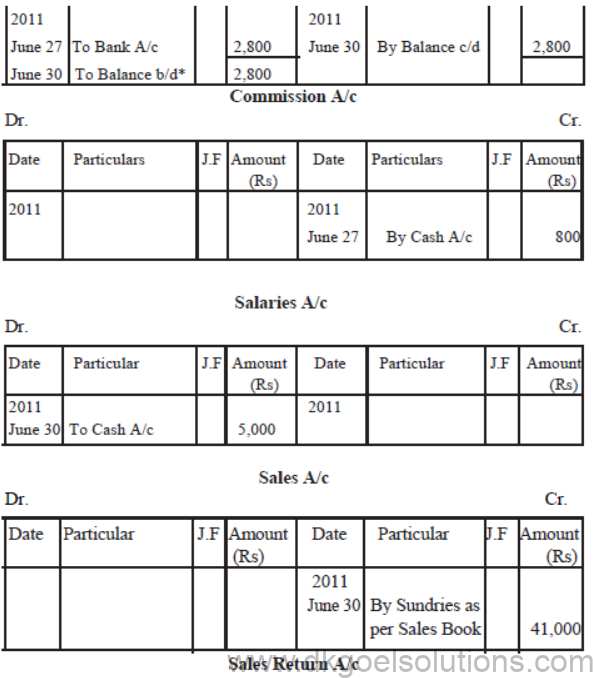

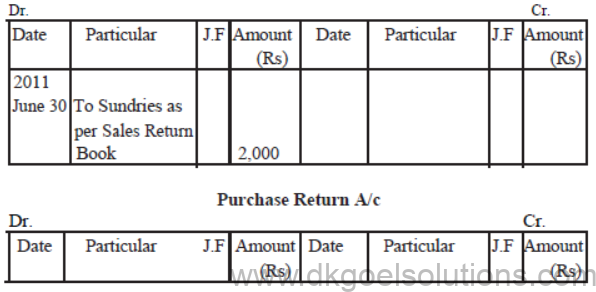

Illusration: Enter the following transactions in proper Subsidiary Books, post them into Ledger Accounts, balance the accounts and prepare a Trial Balance.

2011

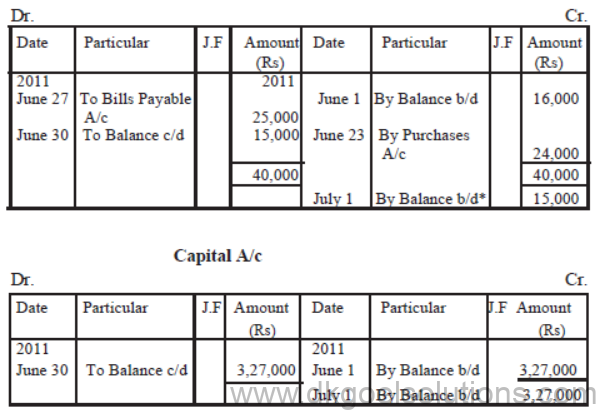

June 1. Assets : Cash in hand Rs. 20,000; Debtors : Amit and Co. Rs. 15,000, Sumit Bros.

Rs. 30,000, Stock Rs. 1,75,000, Machinery Rs. 1,20,000, Furniture Rs. 40,000.

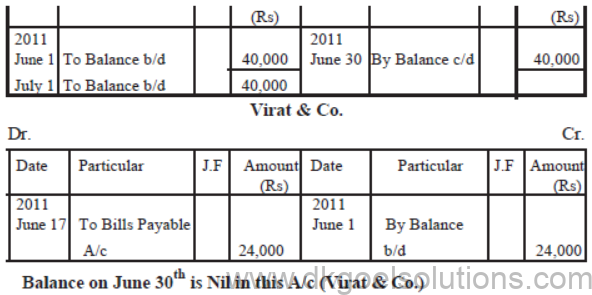

Liabilities : Bank overdraft Rs. 33,000, Creditors : Virat and Co. Rs. 24,000, Vishal Rs. 16,000.

June 2 Purchased from Ramesh and Sons goods of the list price of Rs. 20,000 at 10% trade discount.

June 5 Returned to Ramesh & Sons goods of the list price of Rs. 2,000.

June 10 Issued a cheque to Ramesh and Sons in full settlement of their account.

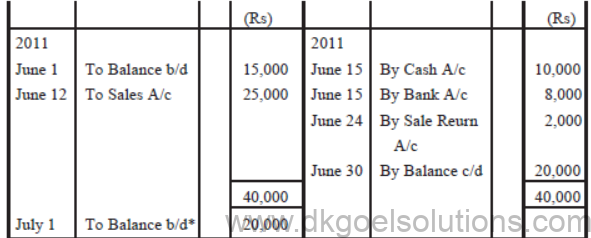

June 12 Sold to Amit and Co., goods worth Rs. 25,000.

June 15 Received cash Rs. 10,000 and a cheque for Rs. 8,000 from Amit and Co. The cheque

was immediately deposited into the bank.

June 16 Withdrawn for personal use cash Rs. 5,000 and goods of Rs. 3,000.

J une 17 Accepted a bill for 45 days drawn by Virat and Co. for the amount due to him.

June 18 Acceptance received from Sumit Bros. for the amount due from them payable after 30 days.

June 19 Sold to Mohit Bros., goods for Rs. 16,000.

June 20 Cash purchases Rs. 15,000.

June 22 Withdrawn from bank for office use Rs. 10,000.

June 23 Purchased from Vishal goods valued at Rs. 24,000.

June 24 Amit and Co. returned goods worth Rs. 2,000.

June 25 Received from Mohit Bros. Rs. 10,000.

June 27 Accepted a bill for Rs. 25,000 for 1 month draw by Vishal.

June 27. Paid by cheque, Rent Rs. 2,800

June 27 Received Commission in Cash Rs. 800

June 30 Paid salaries Rs. 5,000.

SOLUTION:

Notes :

1. Extras marked with will* not be posted anywhere in the ledger.

2. Closing Balances of Cash and Bank will be shown in the Trial Balance.

3. All other A/cs shown in the Debit side will be credited & All other A/cs shown in the Credit side will be debited.

Posting of opening Entries :

Important: Besides opening Journal entries, any transaction which is not covered under any of the Subsidiary Book is done in Journal proper.

Vishal’s A/c

Drawings A/c

Mohit Brothers A/c

TRIAL BALANCE

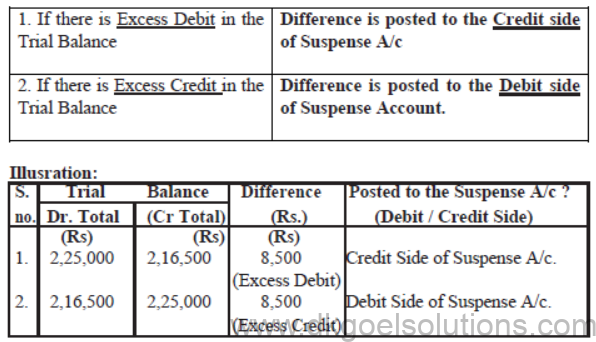

SUSPENSE ACCOUNT

When Trial Balance does not agree, then first of all we try to locate the errors. Sometimes, in spite of the best efforts, all the errors are not located and the Trial Balance does not tally. Then in order to avoid delay in the preparation of final accounts, a new account is opened which is

known “Suspense Account” Difference in Trial Balance is posted to this Account.

Closing of Suspense A/c :

• The errors which led to the difference still remains to have to be located.

• These errors will be rectified through Suspense A/c (One sided errors) which will be explained in the topic Rectification of Errors.

• When all the errors are rectified, this Account closes down automatically. If the difference in Trial Balance persist, it is shown in the Balance Sheet.

Points to be Remember:-

(1) Debit Balance of Suspense Account is shown in the Asset Side of the B/Sheet.

(2) Credit Balance of Suspense Account is shown in the Liability Side of the Balance Sheet.